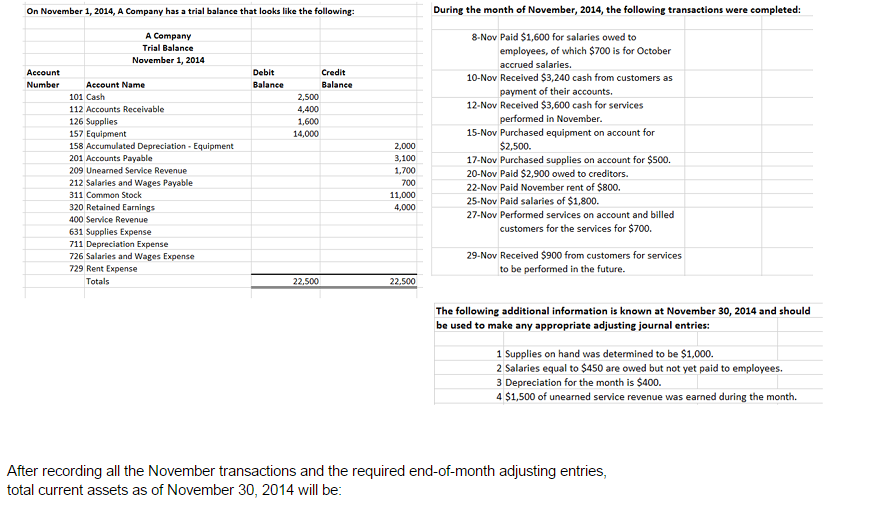

Campus Cycle Shop Trial Balance

Bicycle - Wikipedia. The most popular bicycle model. A bicycle rider is called a cyclist, or bicyclist. Bicycles were introduced in the 1. Europe and as of 2. The following transactions occurred during June for Campus Cycle Shop. Trial Balance Particulars Debit Credit Accounts Payable Cash Equipment.

Initially the game offers over 70 songs, most of which are master tracks.

Hiseman announced his plan to form the band eventually named Colosseum II in November 1974, but only Gary Moore was named as a member. Alan parsons project torrent. Rehearsals were due to begin on January 1, 1975, but a permanent unit was not finalised until May 1975. Among musicians who almost made the group were Graham Bell, Duncan Mackay and Mark Clarke. Colosseum II was a British band formed in 1975 by the former Colosseum drummer and leader, Jon Hiseman, following the 1974 demise of his band Tempest.

What is an Adjusted Trial Balance? An adjusted trial balance is a listing of all company accounts that will appear on the after year-end adjusting journal entries have been made. Preparing an adjusted trial balance is the fifth step in the and is the last step before can be produced. Format An adjusted trial balance is formatted exactly like an unadjusted trial balance.

Three columns are used to display the account names, debits, and credits with the debit balances listed in the left column and the credit balances are listed on the right. Like the unadjusted trial balance, the adjusted trial balance accounts are usually listed in order of their account number or in balance sheet order starting with the,, and and ending with and. Both the debit and credit columns are calculated at the bottom of a trial balance. As with the, these debit and credit totals must always be equal. If they aren’t equal, the trial balance was prepared incorrectly or the journal entries weren’t transferred to the ledger accounts accurately. As with all financial reports, trial balances are always prepared with a heading. Typically, the heading consists of three lines containing the company name, name of the trial balance, and date of the reporting period.

Preparation There are two main ways to prepare an adjusted trial balance. Both ways are useful depending on the site of the company and chart of accounts being used. You could post accounts to the adjusted trial balance using the same method used in creating the unadjusted trial balance. The account balances are taken from the T-accounts or ledger accounts and listed on the trial balance. Essentially, you are just repeating this process again except now the ledger accounts include the year-end adjusting entries.

You could also take the unadjusted trial balance and simply add the adjustments to the accounts that have been changed. In many ways this is faster for smaller companies because very few accounts will need to be altered. Note that only active accounts that will appear on the financial statements must to be listed on the trial balance. If an account has a zero balance, there is no need to list it on the trial balance. Example Using Paul’s and his, we can prepare the adjusted trial balance.

Once all the accounts are posted, you have to check to see whether it is in balance. Remember that all trial balances’ debit and credits must equal.

Now that the trial balance is made, it can be posted to the and the can be prepared.